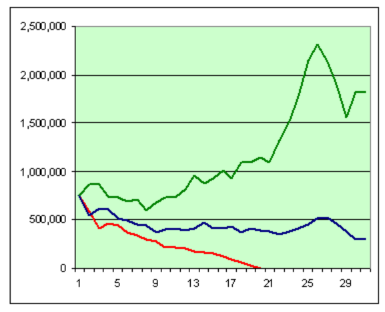

How long will your investment last based on your current needs? The graph above shows an example where $100,000 gets invested in each of the three Canadian account types, Open / RRSP and TFSA, with a mixture of investment return rates, pension fund income, and fixed expenses, incorporating inflation and taxes. You can see it lasts about 30 years into the future, based on one of the retirement income planner (RIP) tools discussed below.

How do you know if your Investment advisor is a “Good” one, or if there is a “better” one, and who is the “best” one is for your needs?

If your investments are producing “good” results (or bad), then how would you know if you could have gotten better results from them if you invested differently?

What do stereo systems have to do with investing?

I learned a valuable lesson in my younger years when I sold component stereo systems (the kind that had a separate record player and speakers, and amplifier/tuner). Since there were an almost unlimited number of combinations of speaker sizes and qualities and turntable types, the store published catalogs which had pre-selected combinations organized as Good / Better / Best to make it easier to select a combination that suits your needs.

The “Best” choice, is not always the most expensive combination for everyone. An older person may prefer the simplicity of a simple all in one system with small speakers that don’t shake the walls.

Banks

For some people using your local bank advisor can be a “good” choice. Their advice is “free” – cookie cutter long term focused type advice, generally limited to the investment products that they are selling, and may require over $100K in investment funds. Typically suited to passive type of investors who want a low risk hands off approach. The services that appear to be “free’ are actually paid for by the class “A” of Mutual fund investments that you are buying.

Independent advisors

A “better” advisor type is probably an independent advisor agency who is willing and able to personalize your investment strategy to suit “your style”. They will tend be familiar with a particular “brand” of investment choices, but should be able to work with a wider variety of choices than a bank can. If you are looking for a higher rate of return, they may also have services that buy and sell investment funds aligned with your risk tolerance. They will typically charge a fee of some sort. It could be a flat percentage for example 1% of your investment portfolio per year. Or it may be paid for based on the commissions associated with managing your investments. There are even a few who simply charge by the hour at rates comparable with a lawyer – hundreds per hour. Better advice costs more money.

Self Directed Investing

The “best” advisor may turn out to be yourself – if you have the time and motivation to educate yourself! Most of the major banks now offer “self directed” investing, which will provide you access to exactly the same mutual funds as the banks will sell you through their investment advisors, but at a cost which is about 1% less than the Class A funds. Typically class D (direct) or F (financial advisors).

Heading into retirement where you suddenly change gears from saving as much as you can, to trying to live on the funds you have accumulated can require careful consideration to consume the funds in a way that is “efficient” from various perspectives. In Canada we have three broad categories of investment account types which have important income tax related differences between RRSP/RIF’s, TFSA and non registered (open) funds as outlined in a brief form below:

| Open / non-registered | Ordinary savings accounts and investments that have not been setup to minimize income tax payable at year end. These types of savings can still incur taxes at different rates depending on the type of investment. For example, for an ordinary bank savings account interest gets charged the highest percentage rate of tax. Stocks / Mutuals and similar investments also require taxes be paid on their growth when sold, but its about 50% of normal interest type investments because of Capital Gains provisions. Some stocks and mutuals will also give “dividends” which are taxed somewhere between the rates for interest and stocks depending on a bunch of factors. |

| RRSP / RIF | Registered Retirement Savings Plans (RRSP) and Retirement Income Funds (RIF) are designed to reduce your income taxes payable at year end, by retaining investments in a special account type which is “registered” with the government tax department. These funds do get taxed when the money is withdrawn from the account, which generally is when your total annual income is likely to be less than when working. Typically, withdrawals are achieved by converting the RRSP into a RIF account, but it does not have to be done this way. |

| TFSA | Tax Free Savings accounts, are a different type of “registered” account that allows you to grow your investments, WITHOUT paying income tax on the growth of your money! You don’t get a reduction in taxes when you contribute to the account, but when you withdraw money from the account, no additional taxes need to be paid. Therefore these accounts are generally best used for your highest growth type of investments. There is a maximum cap that is allowed to be kept in this account type, which increases each year by $5,000 or so. It is important not to exceed the cap, because there are substantial financial penalties if you do. |

| USA | USA and Canada use different terminology for similar tax saving related account types. My understanding from a Canadian perspective is that the USA IRA (Individual Retirement Account – 401/K) is similar to Canada’s RRSP, and the Roth IRA is similar to Canada’s TFSA. |

In retirement, you will need to decide which account to draw from in what order, or combinations of all three at the same time. A common approach is Open first, then RRSP/RIF, then TFSA, but there are nine different permeations of these three account types which can make the decision confusing.

Retirement Income Planning (RIP) calculators

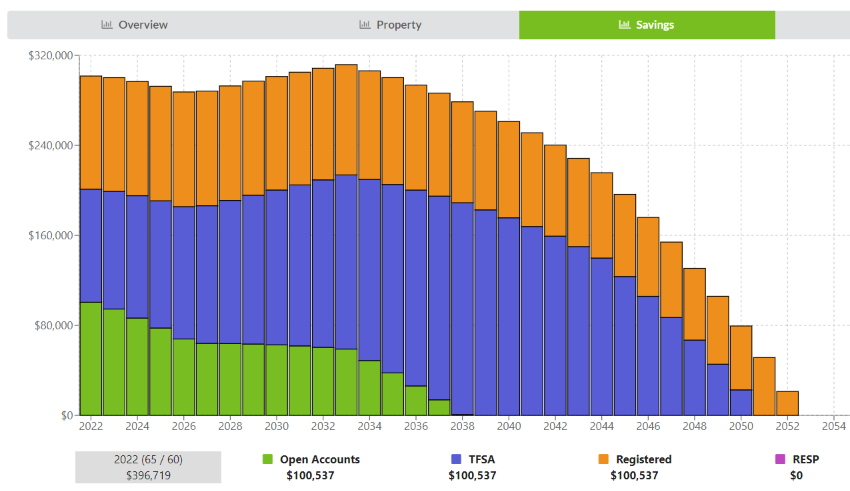

There are various ways to calculate and project your monthly retirement income based on all or some of the many factors. Most of the free investment advice web sites have a very simple model, which just give a general idea using a few key parameters (e.g. Annual spending, portfolio value, number of years) But since investing is a long term thing, being able to project 30 years or more ahead based on small changes you make today, which can have a big effect, is important.

The one I am currently using incorporates “everything” into one easy to use model, for a small monthly / annual fee. Link to their site: Better Money Choices

It includes:

- The dollar amounts you have in each of the three investment account types (RRSP/RIF, TFSA, Non registered), and their expected percentage return percentage. e.g. 5%

- Pension or other income sources, including dividends from stocks.

- Expected monthly expenses

- Special expenses – like budget for travel or household maintenance, Education savings plans for grandchildren, etc.

- Factor for inflation (e.g. 2%)

- Real Estate assets, and expected growth percentage.

It has many graphs and the ability to export to excel.

Another contender for Canadians is Money Ready You can use it for free for three calculations, but I ran out of free runs before I could form an accurate opinion about it for my use.

Americans may want to investigate this “free” one, that I considered, but without the Candian Tax rules.

FIRECalc: A different kind of retirement calculator